How to Calculate Operating Income? (Formula & Examples)

Table of Contents

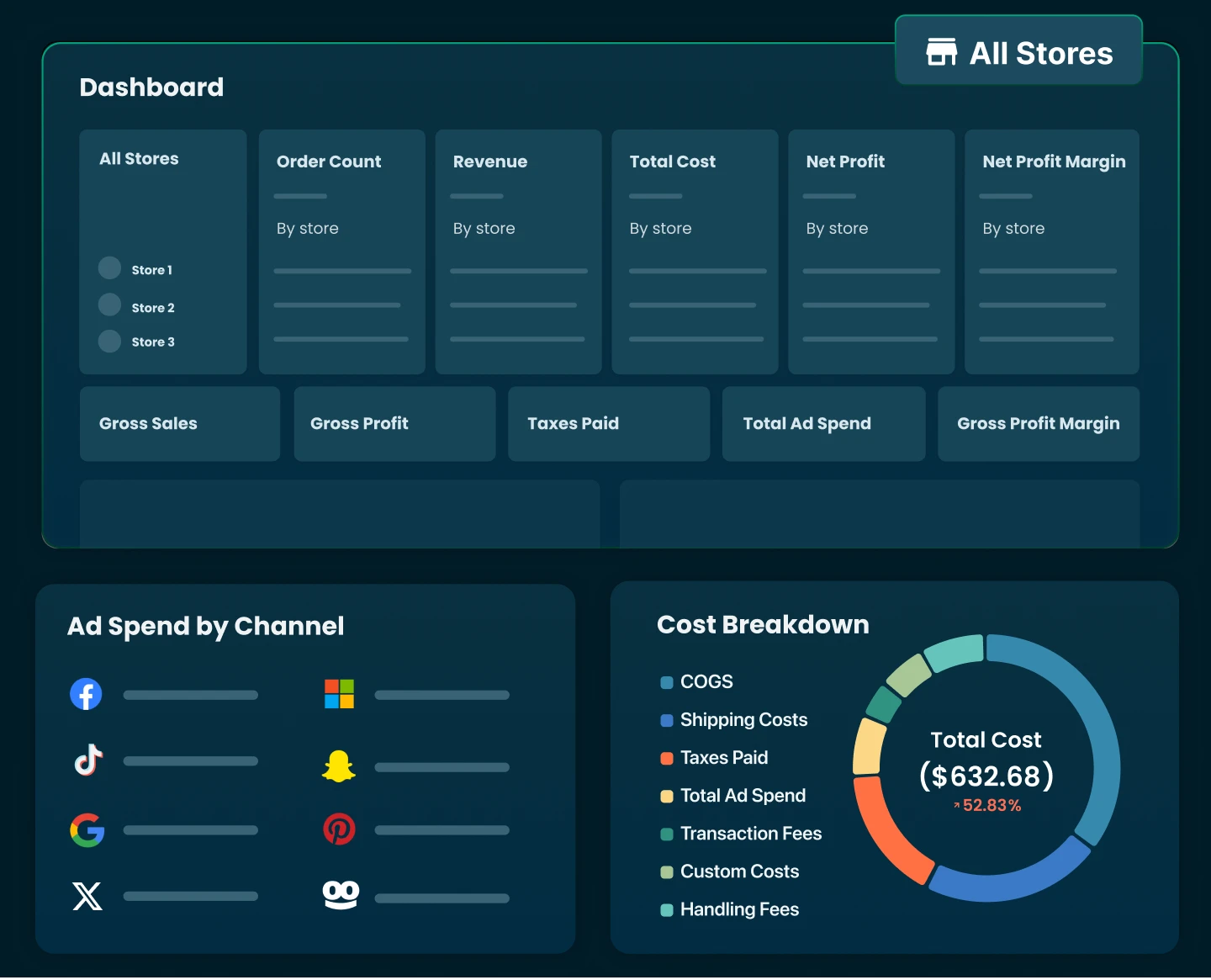

Operating income is a key ecommerce metric that shows how much profit your Shopify store makes from its core business operations. It tells how much you earn after deducting product costs and business expenses like marketing, app subscriptions, and employee salaries.

In this blog:

Operating Income Formula: How to Calculate It

The operating income formula is:

To break it down further:

Operating Expenses include store-related costs such as Shopify fees, marketing expenses, salaries, and shipping costs.

Operating income is also known as Earnings Before Interest and Taxes (EBIT) because it focuses only on the revenue and costs directly tied to running your store.

Image source: Amazon’s Consolidated Statements Of Operations

Sample Calculation of the Operating Income Formula

Let’s say you run an online store selling custom apparel. Here’s an example of how you’d calculate operating income:

- Total Revenue: $50,000

- Cost of Goods Sold (COGS): $20,000 (includes product sourcing and manufacturing)

- Gross Income: $50,000 - $20,000 = $30,000

- Operating Expenses: $10,000 (marketing, Shopify apps, shipping, rent, salaries)

- Operating Income: $30,000 - $10,000 = $20,000

In this case, your store generates $20,000 in profit from operations before taxes and interest.

What are Direct and Indirect Costs?

Understanding your costs is crucial for accurate profit calculations and customer profitability analysis. Your Shopify store’s expenses fall into two main categories:

- Direct Costs (COGS): These are costs directly tied to product sales, such as wholesale product costs, manufacturing, and shipping fees.

- Indirect Costs (Operating Expenses): These include expenses like advertising, website hosting, software subscriptions, and customer service wages.

Knowing the difference helps you allocate resources effectively and improve profitability.

Operating Income = EBIT

EBIT (Earnings Before Interest and Taxes) is another term for operating income. It excludes financing costs, making it a reliable indicator of your store’s operational efficiency.

If your Shopify store has high revenue but low operating income, it may be a sign that your expenses are eating into profits.

Why is the Operating Income Important for Your Shopify Business?

Understanding your store’s operating income helps you make informed financial decisions and optimize profitability. By analyzing this metric, you can:

- Evaluate Profitability: It helps you see if your store is making real profit from selling products, not just generating revenue. Check this article to understand the key difference between net profit vs. revenue.

- Guide Pricing Strategies: If your operating income is low, you may need to adjust product pricing strategies or reduce costs.

- Attract Investors or Loans: A strong operating income makes your store more attractive to potential investors or lenders.

- Help With Business Growth: Understanding operating income allows you to reinvest wisely into ads, product expansion, or improving customer experience.

Want to go beyond operating income and see your true net profit? Use our free Net Profit Margin Calculator to instantly measure your store’s financial health. Simply enter your revenue, COGS, and expenses to get a clear picture of your profitability. Try it now

Understanding operating income formula is essential for evaluating a company's core profitability and making informed business decisions.

By using the 2025 formula and real-world examples, you can gain clearer insights into operational efficiency and financial health. Whether you're a business owner, investor, or student, mastering operating income helps you analyze performance beyond the top line.

Tracy is a senior content executive at TrueProfit – specializing in helping eCommerce businesses scale profitably through content. She has over 4 years of experience in eCommerce and digital marketing editorial writing. She develops high-impact content that helps thousands of Shopify merchants make data-driven, profit-focused decisions.

![Amazon Profit Margin: Every Detail You Should Know [2026]](https://be.trueprofit.io/uploads/amazon-profit-margin-68931b2607c12.webp)